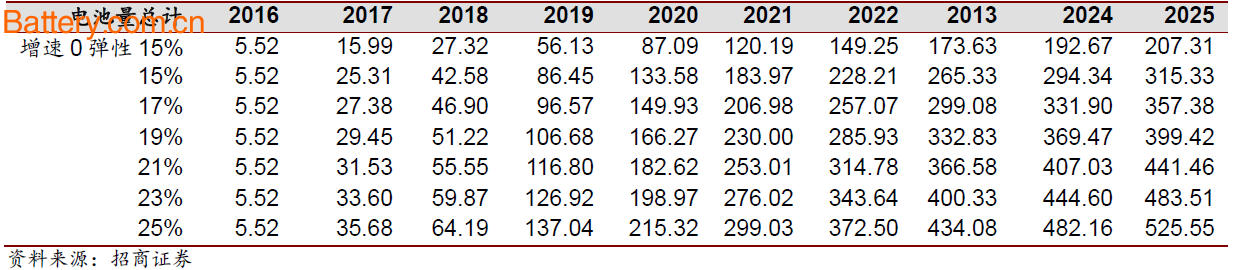

A few days ago, China Merchants Securities released an analysis report that “new energy vehicles will welcome global heavy volume and upstream supply and demand will continue to be tightâ€. In the report, China Merchants Securities analysis believes that the short-term status of ternary yuan will not change, and the comprehensive popularization of 811 technology will take time, and it will become the mainstream of power battery in the future; after 2019, lithium metal and cobalt will continue to be tight, due to raw materials. The price rises, and the lithium battery will move toward 811 technology. The short-term status of ternary yuan will not change, and it will take time for 811 technology to be fully popularized. Ternary materials are currently the best choice for power batteries. Since the popularization of lithium-ion battery technology, a variety of battery systems have appeared in the academic world, but from the practical point of view, at present, the anode material is mostly graphite, and the cathode material is lithium cobaltate, lithium iron phosphate, ternary, Materials such as lithium manganate. Power batteries require materials with high energy density (corresponding to high cruising range) and high safety, while lithium cobalt oxide is not suitable for power battery because of its worst thermal stability (poor safety) (but with high pressure Density and energy density are currently the mainstream in the 3C field, while lithium manganese oxide has a low energy density and limited application. Lithium iron phosphate is an early development technology with the advantages of excellent safety, environmental protection and high cycle life, but the disadvantage is energy. The density is low and it is close to reaching the ceiling, and the ternary itself has the advantage of high energy density cap. In the future, as the technology continues to advance, the safety issue will gradually improve. Before other battery technologies fail to achieve major breakthroughs, the ternary is still the driving force. The best choice in the battery field. There is still a bottleneck in the short-term popularity of high-nickel ternary, and it will become the mainstream of power batteries The ternary material refers to a layered nickel-cobalt-manganese composite material (manganese can also be replaced by aluminum, Panasonic NCA technology), and the ternary material undergoes a synergistic effect of Ni-Co-Mn (Ni increases specific capacity, Co enhances ion conductivity and Rate performance, Mn stabilized structure) combines the advantages of three materials: good cycle performance of LiCoO2, high specific capacity of LiNiO2 and high safety and low cost of LiMnO2. Cobalt mainly plays a role in improving conductivity and rate performance, and provides partial capacity at high voltage, playing a key role in the ternary material system. According to the ratio of nickel-cobalt-manganese, the ternary can be divided into 111, 523, 622, 811, etc. Since the main role of nickel is to increase the energy density, the research and development of high-nickel ternary materials (such as 622/811) has become a hot spot. In terms of manufacturers, at present, China is generally developing R&D 622 and 811 technologies, and has not yet mass production. From the perspective of foreign countries, only Panasonic and several other leading companies have high-nickel ternary mass production technology (Panasonic NCA Tesla supplies, NCA ratio 8:1.5:0.5). From a technical point of view, as the nickel content in the ternary material increases, the Ni+2/Li+1 ion mixing is intensified, and the structural stability of the material is lowered, resulting in a significant reduction in cycle life and safety. China Merchants Securities summarized the reasons why the domestic high-nickel ternary is difficult to spread in the short term. From a technical point of view: high nickel ternary with the increase of nickel ratio, nickel-lithium ion mixing and exacerbation, Ni + 2 mixed in the Li layer, reducing the discharge specific capacity, hindering the diffusion of lithium ions; at the same time due to nickel in the deintercalation of lithium The phase change in the process leads to obvious volume change, which makes the structural stability of the material worse and the cycle life decreases. The surface of the high nickel positive electrode is more likely to form impurities such as lithium carbonate (the nickel content increases more than 60%), and thus occurs with the electrolyte. The side reaction reduces the cycle life, and the high temperature will cause the flatulence; as the nickel increases, the thermal stability of the positive electrode material decreases, and the exotherm increases, the thermal stability of the material becomes worse; different material systems need to match different electrolyte formulations, while high nickel three Due to the increase of surface impurities, it requires a more optimized electrolyte formulation, and from the domestic technology, the electrolyte matching problem is also a big problem. From the application point of view: high nickel ternary materials due to its inherent properties such as structural instability, thermal stability and cycle life are poor, from the current domestic manufacturers research and development progress, currently not fully resolved the safety of high nickel materials in practical applications Sexual problems; because high-nickel ternary materials can not contact the air during battery assembly, a pure oxygen atmosphere is required, and since domestic battery companies start from the ternary NCM111, the NCM111 assembly does not require a pure oxygen atmosphere, so the domestic battery factory almost There is no oxygen burning process, and in order to mass produce NCM811, it is necessary to redesign the plant and equipment, and the backwardness of the equipment manufacturing process is also a major problem that restricts the mass production of NCM811. Permeability 15%-25% in 2025 Lithium supply curve: According to preliminary statistics, in 2016, the global lithium carbonate used for power batteries was 42,600 tons, equivalent to 0.5 million tons of lithium equivalent, and the expected output of new lithium carbonate was 50,000 tons/year in the next five years, equivalent to lithium. With an equivalent weight of 0.38 million tons, we make the extreme assumption that the future lithium supply increments are all applied in the field of power batteries (in other applications, the increment is 0), and finally the lithium supply curve is obtained. Cobalt supply curve: According to preliminary statistics, the global refined cobalt production in 2016 was 101,700 tons, while the cobalt used in the field of power batteries was about 6,000 tons. Considering the existing situation of cobalt as an associated mine, under the existing conditions, each year The new cobalt production limit is about 10,000 tons. The same extreme assumption is that the future cobalt supply increments are all applied in the field of power batteries, assuming that the cobalt production is increased by 0.8 million tons per year and the annual increase of 10,000 tons in 2019. That is, two supply curves of cobalt supply 1 and cobalt supply 2 are provided. Elastic demand curve: The elastic demand curve counts 15-25% of the world's top 10 automakers' total passenger car sales in 2025, with values ​​of 15%, 17%, 19%, 21%, and 23 respectively. %, 25% as the elasticity value (as a comparison, the growth rate is 0% elastic 15% extreme, that is, the total sales volume of each manufacturer in 2016 is 2025 sales), thereby measuring the sales volume of new energy vehicles of various manufacturers in 2025 (2025 total sales volume) According to the actual growth rate of each manufacturer, we estimate the growth rate of new energy vehicles in 2016-2025 according to the actual sales situation of each manufacturer, and get the sales forecast for each year. Finally, the proportion of EV and PHEV produced by each manufacturer in 2016 and The amount of bicycle battery (which is not averaged) is standard, and it is assumed that the EV ratio in 2025 is 80%, which is calculated from the total battery demand under different elastic conditions from 2017 to 2025, and then the lithium and cobalt according to the 1kWh battery. The content of the measurement corresponds to the demand for lithium and cobalt. The battery is assumed to be all ternary 622 or 811: Considering that most of the international manufacturers' passenger cars take the ternary route, the battery energy density will be further improved in the future, and there will be a shift from the ternary 622 to 811 technology path in the future, so all the assumptions are assumed for the total demand. For the two extremes of ternary 622 and ternary 811, that is, the total demand of the top 10 manufacturers 2017-2025 battery multiplied by the lithium and cobalt content of the unit battery to obtain the demand curve for lithium and cobalt under different elasticity in 2017-2025. Cobalt and lithium supply will have a big gap in the future Lithium resources will be in short supply in 2019-2021. According to the previous assumptions, as the world's top ten automakers' new energy vehicles begin to accelerate in 2019, the demand for lithium resources has also exploded, corresponding to 15% and 25% of demand. Elasticity, lithium supply began to fall short of supply in 2019 and 2021, and considering the lag of upstream resources (it takes a while to develop new energy vehicles from lithium resources), the time for supply shortage may be advanced. At the same time, this demand is only the demand for raw materials for new energy vehicles of the world's top 10 traditional automakers. It does not consider Tesla , BYD and other enterprises, so lithium resources will start to shortage before 2019. The shortage of cobalt resources is forced to develop from the ternary to the 811 path. From the elastic supply curve of cobalt, it can be clearly seen that the supply and demand of the ternary 622 path and the ternary 811 path cobalt are completely opposite. If the demand is all ternary 622, the cobalt is In the 2019-2021 interval, there will be a shortage of supply, and if the demand is all ternary 811, the cobalt supply can meet the demand. By measuring, for the case of cobalt supply 1, when the ratio of ternary 811:622 reaches 8:2, cobalt can reach the supply balance. China Merchants Securities believes that due to the small elasticity of cobalt supply, if the mainstream manufacturers choose the ternary 622 route, they will face a serious shortage of cobalt supply in 2019-2021. Therefore, the supply of cobalt will force the future of new energy vehicles. The ternary 811 path develops. Through the analysis of cobalt and lithium elastic supply and demand balance table, only the demand for raw materials of new energy vehicles of the world's top 10 traditional automakers (excluding Tesla, BYD, etc.) will be in short supply in 2019-2021, although there is currently a domestic presence. The upstream cobalt and lithium resources are over-represented, but with the gradual increase in the number of new energy vehicles in the world's top ten traditional car companies, there will still be a large gap in the future of cobalt and lithium resources. Vibrating Screen,Vibrating Screen Filter,Dry Separation Screener,Vibrating Control Screener Xinxiang Zhenying Mechanical Equipment Co., Ltd , https://www.beltconveyor.nl

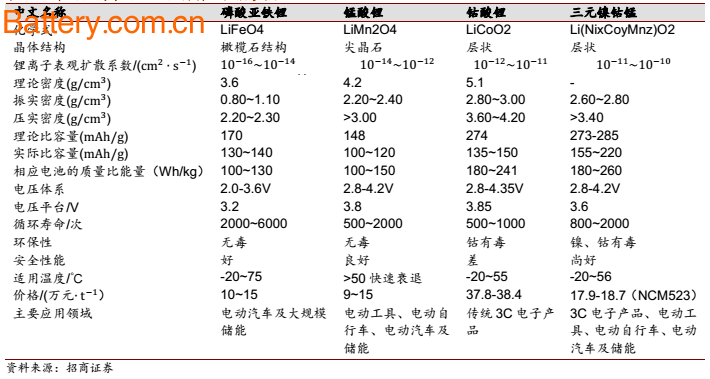

Common lithium ion battery cathode materials and performance parameters

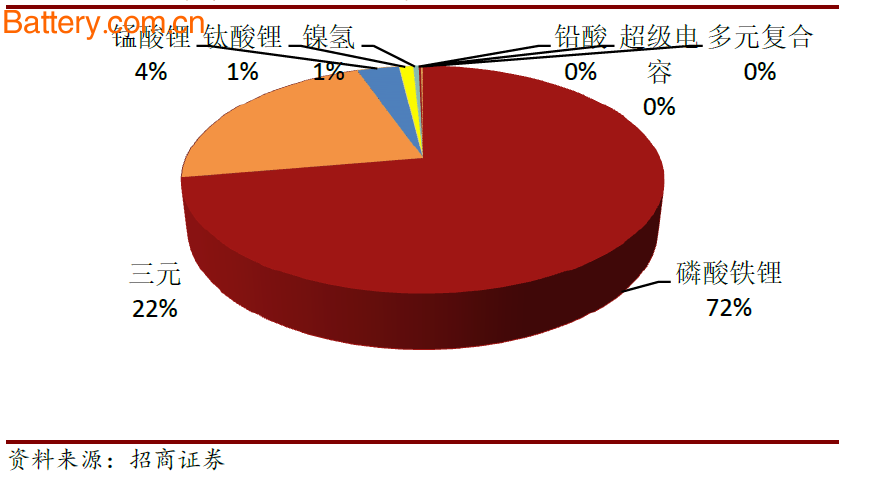

2016 China's power battery shipments by battery ratio

Relationship between specific capacity, thermal stability and capacity retention of ternary materials with different components

Estimation of total battery demand for the top ten groups in 2017-2025 (GWh)